Updated June 2026

What Is Liability Insurance Insurance?

Liability insurance is the only auto coverage Florida law requires. It pays when you cause an accident and someone else gets hurt or their property gets damaged. Bodily injury liability covers medical bills, lost wages, and legal fees for people you injure. Property damage liability covers repair costs for vehicles, buildings, or other property you damage. Your own injuries and vehicle damage are not covered — liability only protects others.

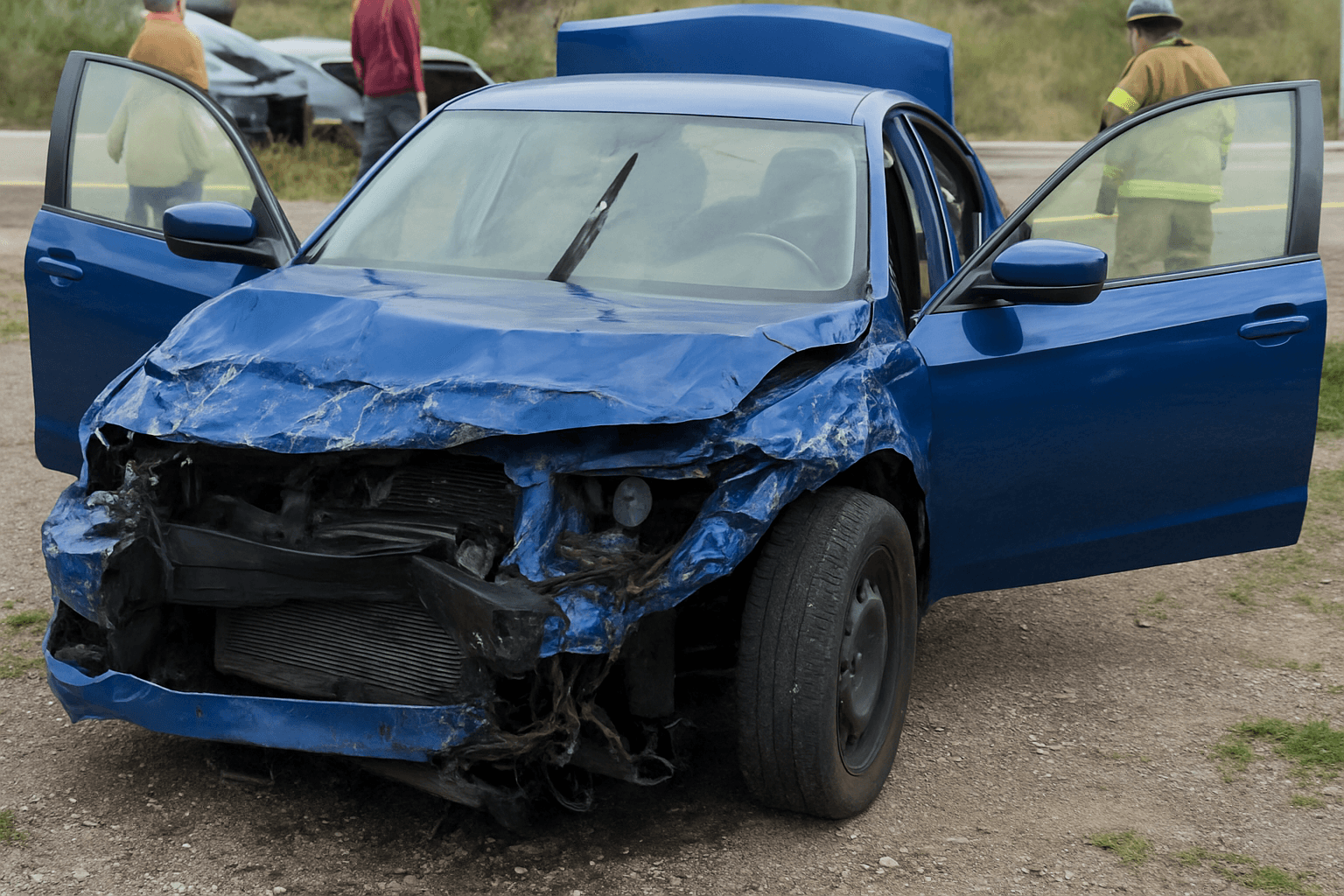

- You rear-end a car at a stoplight. The other driver has $8,000 in medical bills and their vehicle needs $6,500 in repairs. Your bodily injury liability pays the $8,000 in medical costs. Your property damage liability pays the $6,500 in vehicle repairs. Your own vehicle damage is your responsibility — liability does not cover it.

- You cause a three-car accident. Two people have combined medical bills of $45,000 and total property damage is $22,000. If your bodily injury limit is $25,000 per accident, you owe the remaining $20,000 out of pocket. If your property damage limit is $10,000, you owe $12,000 for the vehicle repairs yourself. This is why suspended drivers often need higher limits than Florida's minimum.

- You carry Florida's minimum $10,000 property damage limit and total a vehicle worth $28,000. Your liability coverage pays $10,000. The other driver can sue you personally for the remaining $18,000. Florida allows drivers to carry minimal liability, but reinstatement after suspension often requires proof of higher limits or an SR-22 filing with more robust coverage.

Who Needs Liability Insurance Insurance?

Liability insurance is required for all Florida drivers, including those reinstating after suspension. You must carry it to satisfy SR-22 filing requirements, hardship license conditions, and full reinstatement. If you do not own a vehicle, a non-owner liability policy fulfills the same legal requirement and costs $40–$80 per month.

If you are applying for reinstatement or a hardship license, you need liability coverage now — the state will not process your application without proof of insurance or an SR-22 filing. If you own a vehicle, carry at least $25,000/$50,000 bodily injury and $25,000 property damage to avoid personal liability exposure. If you do not own a vehicle, get a non-owner policy to satisfy the requirement without paying for vehicle coverage you do not need.

How Much Does Liability Insurance Insurance Cost?

Liability-only policies in Florida for suspended drivers typically cost $120–$180 per month, or $1,440–$2,160 per year. Drivers with DUI suspensions or multiple violations pay $180–$280 per month.

- Violation history — DUI, reckless driving, and hit-and-run suspensions increase liability premiums by 60–120% compared to clean-record drivers.

- SR-22 filing requirement — adding SR-22 proof-of-insurance filing typically adds $15–$35 per month to liability premiums.

- Liability limits selected — increasing bodily injury coverage from $25,000/$50,000 to $100,000/$300,000 adds $30–$50 per month.

- Length of suspension — drivers reinstating after suspensions longer than 12 months face higher rates for the first policy term.

- County of residence — Miami-Dade and Broward County drivers pay 20–35% more for liability than drivers in rural counties due to accident frequency.

- Credit-based insurance score — Florida allows insurers to use credit history, which affects liability rates by 15–40% even for minimum coverage.